CPI January 2021

17 Feb 2021

Higher inflation in January confirms expectations of more increases on the horizon

Base effects and electricity tariff adjustments will see inflation rise notably in coming months.

Statistics South Africa (Stats SA) reported on February 17 that consumer price inflation increased from 3.1% y-o-y in December 2020 to 3.2% y-o-y in January 2021. The latest number was slightly below expectations (3.3% y-o-y) and remained near the bottom end of the South African Reserve Bank (SARB) target range (3%-6%). Food and non-alcoholic beverages inflation eased by 6.0% y-o-y in December to 5.4% y-o-y in January as the prices of fish, vegetables, cold beverages and ‘other foods’ declined between the two months.

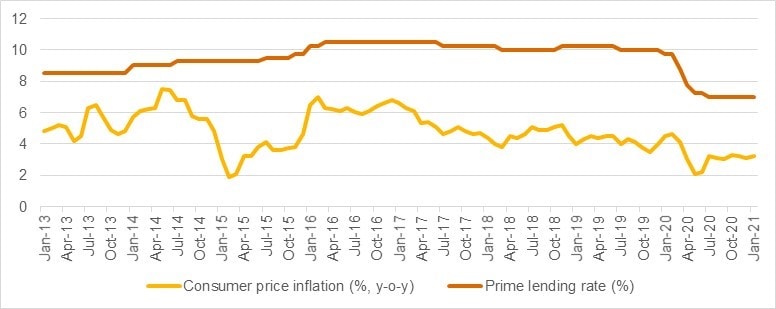

Figure 1: Inflation and interest rates remain low but with higher levels on the horizon

Sources: Stats SA, SARB

Retail price pressures have been below-average during the lockdown. Over the period April 2020 – January 2021, consumer price inflation averaged only 2.9%. Amidst an economic recession, with dampened consumer demand due to a significant decline in employment, retailers were unable to pass on supply-side cost increases to consumers.

In other cases, certain companies were able to avoid increasing their service tariffs due to significant changes in their operating costs. For example, several medical insurance providers did not implement annual price increases in January 2021. This was due to a significant change in healthcare consumption patterns last year resulting in an increase in their cash reserves.

However, the rate of inflation is expected to increase in the near-term, with the SARB forecasting in January that headline inflation will average 4.5% during the second quarter. Of course, this figure includes some substantial base effects from the disinflation seen during the April-June 2020 period. However, there are other real risks to the price environment. As the central bank’s Monetary Policy Committee (MPC) commented last month, in the absence of demand side pressures on retail prices, electricity and other administered prices “remain of serious concern”.

Indeed, the Gauteng high Court ruled this week that Eskom will be able to lift its tariffs by more than 15% this year.

Following the MPC meeting in January, SARB Governor Lesetja Kganyago commented that the central bank’s internal modelling suggested a start to monetary policy tightening as soon as the second quarter of 2021. At the time, we argued that a 3:2 split in MPC votes in January - with two members seeking a rate cut and the other three preferring a ‘hold’ decision – suggests it is unlikely that the MPC will shift towards rate hikes as quickly as the second quarter.

On a further positive note, Kganyago said early in February that the SARB has scope to respond with further support should a third wave of COVID-19 infections hit South Africa this year. All three of PwC’s economic scenarios (baseline, upside and downside) factor in a third wave of infections and varying degrees of stricter lockdown levels during winter 2021.

The next MPC meeting is scheduled for March 23-25. Before then, the SARB will see key information released that should help refine its near-term outlook for the economy. These include Budget 2021 as well as gross domestic product (GDP) and employment data for 2020Q4..