South Africa’s major banks maintained a steady growth path in 2024 amidst a challenging operating climate and significant macro and geopolitical related uncertainty

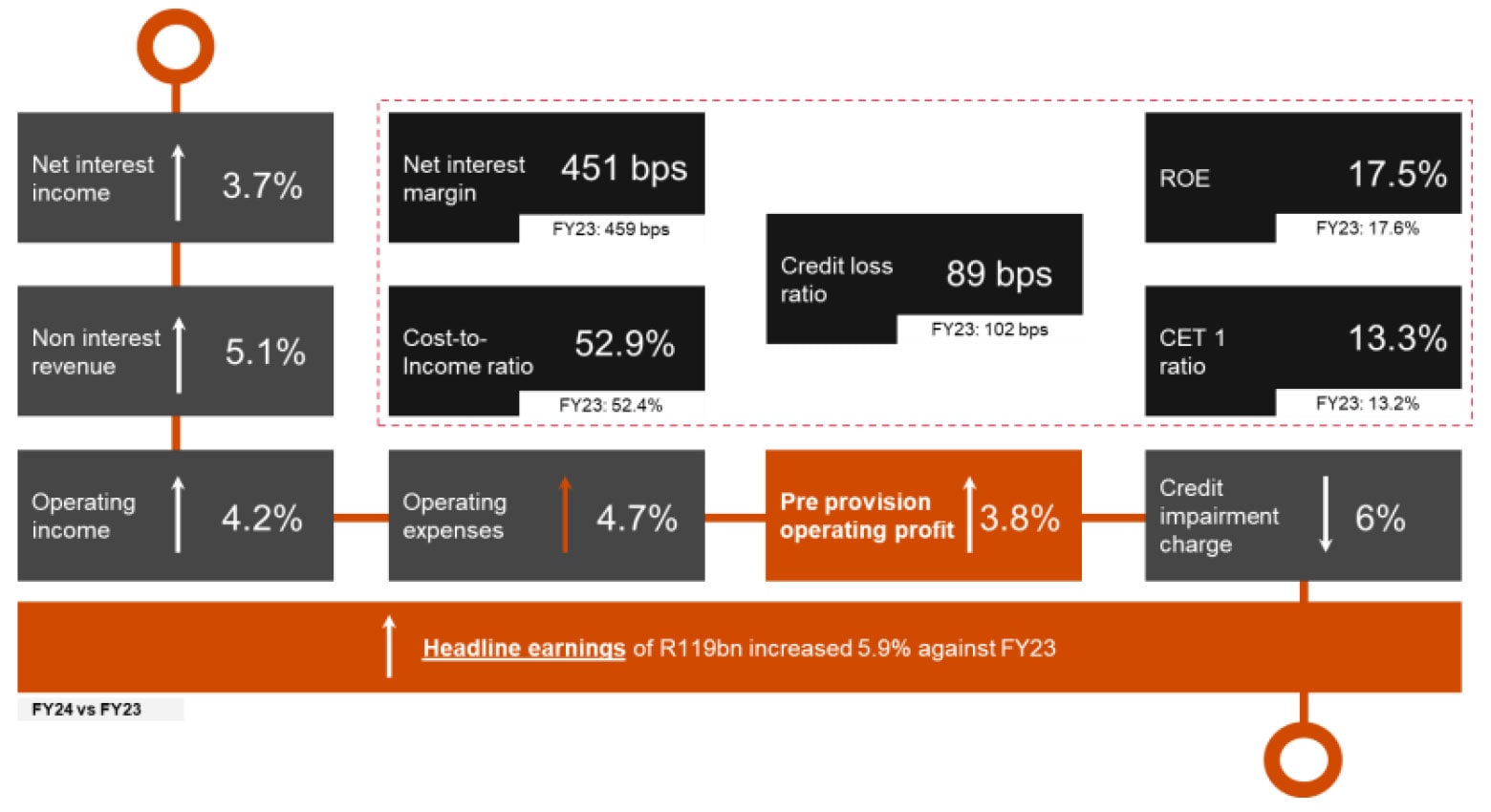

Combined headline earnings growth of 5.9% against FY23 to R119bn, combined ROE of 17.5% (FY23: 17.6%), net interest margin of 451 bps (FY23: 459 bps), credit loss ratio of 89 bps (FY23: 102 bps), cost-to-income ratio of 52.9% (FY23: 52.4%), common equity tier ratio of 13.3% (FY23: 13.2%)

The year 2024 was a turbulent period for global and regional economies, marked by heightened uncertainty, geopolitical tensions and shifting trade dynamics. Nearly half the world’s population participated in elections, creating a ripple effect of political and economic unpredictability. Global inflation moderated but remained high in many emerging markets, delaying anticipated interest rate cuts, placing strain on fiscal positions in several developing economies and complicating economic recovery efforts. In sub-Saharan Africa, the combined impact of persistent socio-economic challenges, adverse weather patterns, volatile commodity prices and fiscal challenges continued to strain economies, while currency volatility and inflationary pressures persisted.

South Africa, however, saw some positive developments. Steps towards structural reforms, particularly in energy supply and logistics, began to yield results, while the formation of a Government of National Unity was met with cautious optimism by markets. These factors contributed to a stronger rand and relatively improved investor sentiment. Despite these improvements, the South African economy faced headwinds, with high unemployment levels and subdued real GDP growth of 0.6% in 2024.

Against this backdrop, South Africa’s major banks continued to demonstrate their resilience, navigating these and other complex conditions with strategic agility.

"2024 has been another testament to the strength and adaptability of South Africa’s banking sector. Despite continuing and evolving challenges in the global, regional and domestic operating environment, the major banks’ management teams remained focused on delivering value to customers, managing risks and investing in future growth opportunities.”

Key themes emerging from PwC’s analysis of the major banks’ full-year 2024 performance include:

- Solid foundations: The major banks’ balance sheets remain anchored by robust capital and liquidity positions, with solid buffers beyond regulatory requirements supporting risk-taking and strategic investments. Driven by accounting standards and strong risk management, credit provisions kept pace with balance sheet growth, capturing forward-looking information and risk trends in credit portfolios. Credit performance in 2024 showed some signs of improvement with the combined credit loss ratio declining to 89 basis points for the year, down from 102 basis points in 2023.

- Digital transformation and cost efficiency: The shift to digital banking platforms accelerated further, particularly in retail banking, with the number of digitally active clients at 21 million now approaching a third of the South African population by year-end. Investments in technology (both new-build systems and legacy systems enhancement), cloud-based solutions and cybersecurity remained priorities, alongside investments in emerging technologies such as open banking and artificial intelligence. The aggregate cost-to-income ratio edged higher to 52.9%, reflecting lagging inflationary pressures within the overall cost base particularly in the first half of 2024.

- Balance sheet growth and earnings resilience: Steady growth in lending (5.4%) and deposit-taking (8.7%) provided the foundation to support earnings growth in 2024. Supported by larger balance sheets and increased customer numbers, core banking activity revenues saw good growth, while differing experiences were felt in the major banks’ trading businesses given divergent strategies and financial market volatility. Additionally, improved credit trends, particularly in retail lending portfolios, translated to lower credit impairments and supported overall earnings growth.

- Sub-saharan Africa remains central to overall bank strategy: While individual approaches to the rest of the continent vary, capturing significant financial services opportunities among young, mobile and digitally-savvy African populations in high-growth markets remains a central element of the major banks’ strategies. Banks that operate at scale on the continent saw strong underlying growth and constant currency performance in several West and East Africa territories, and continue to diversify their businesses, brands and revenue streams in these key markets. However, regulatory challenges, economic constraints (including inflationary pressures and elevated fiscal and sovereign risks in certain territories) and significant currency volatility dampened results in rand terms. Despite these operating challenges, competing purposefully with a pan-African focus remained a critical component of the major banks’ growth strategies. This sentiment is echoed in our 28th Annual Global CEO Survey – Sub-Saharan Africa perspective which notes that “businesses in Sub-Saharan Africa are undergoing a transformation, driven by demographic changes, technological advancement and the rise of entrepreneurial leadership”.

- Sustainability, emerging technologies and innovation: The major banks made strides in aligning their strategies with sustainability goals, particularly in mobilising funding towards sustainable financing and climate transition initiatives. At the same time, they continue to confidently explore the potential of emerging technologies, such as generative AI, to enhance operational efficiency, risk management processes and customer experiences across a wide range of use cases. These use cases span credit risk management (credit scoring, dynamic market analyses and enhanced risk monitoring at client and portfolio levels), operational and compliance risk management (in areas from data capturing, transaction monitoring and screening, fraud detection and strengthening cyber defenses) and customer experiences (enabling rapid, streamlined and personalised processing of queries and development of personalised propositions and services). This is consistent with what we’ve observed globally within the banking industry—the banks that harness the power of AI, data, and highly qualified people are the ones that are transforming their operations, elevating customer experiences and exceeding stakeholder expectations.

Major banks’ results highlights: PwC’s Major Banks Analysis highlights key themes from the combined local currency results of Absa, FirstRand, Nedbank and Standard Bank, and provides reflections from the common strategic themes within other South African banks. At 31 December 2024, the South African operations of the major banks included in our analysis comprised 83% of total banking sector assets in South Africa (based on BA900 industry data).

“South Africa’s major banks results in 2024 reflect the focused execution of their strategies despite challenging trading conditions and significant levels of uncertainty. The major banks appear to have navigated the risks and challenges facing their businesses and markets of operations to deliver a resilient financial performance. Looking ahead, while complex geopolitics and trade tensions pose elevated macroeconomic headwinds, core focus areas of the major banks are likely to remain on maximising growth vectors and customer experiences, while embedding emerging technologies.”

- Headline earnings: The major banks’ combined headline earnings growth of 5.9% against FY23 to R119bn far surpassed South African and sub-Saharan economic growth. Underpinning earnings growth was the combination of resilient revenue growth across net interest income (3.7%) and non-interest revenue (5.1%), supported by credit impairment charges falling 6%.

- Loan growth: Notwithstanding recovering consumer and business confidence levels from a period of high inflation and interest rates, new loan formation reflected relatively improved conditions in 2024, particularly in the second half. Aggregate gross loans and advances grew 5.4% against FY23 (2% against 1H23). Consistent with previous periods, growth in individual loan portfolios and industry sectors was differentiated between the major banks, based on a combination of differing strategies, geographic footprint and risk appetite. According to Bureau information from the National Credit Regulator (NCR), the number of credit-active South African consumers increased to 28.32 million as at the end of September 2024, growing 3.3% year-on-year.

- Credit quality: As we noted previously, the composite relationship between interest rates and impairments has been well-established. While this dynamic continued, albeit with interest rate cuts of 50 basis points to 7.75% by the South African Reserve Bank (SARB) in 2024 (followed by a further 25 basis points in January 2025), the major banks benefited from provision releases in FY24 following the successful restructure of legacy corporate non-performing loans and a slowdown into early arrears and defaults in South African retail credit portfolios. The combined credit loss ratio (the income statement impairment charge divided by average advances) moderated to 89 bps (FY23: 102 bps) as the income statement bad debt charge decreased 6% for the same period. Total non-performing loans increased 3% against FY23, comprising 5.3% of gross loans and advances (FY23: 5.4%). According to the NCR Bureau information referenced above, the number of South African consumers with impaired records in Q3-24 decreased by 65,094 to 10.2 million, while consumers classified in good standing increased by 237,246 to 18.13 million.

- Costs: Reflecting on inflation data for 2024, Stats SA notes that “the average inflation rate for the year was 4.4%, down from the average of 6.0% in 2023. Inflation in 2024 was the lowest in four years since the pandemic in 2020, when the average rate was 3.3%.” Outside South Africa in the rest of the continent, inflation remained sticky across several key territories in which the major banks operate, influenced by a variety of factors. Against this context, cost control remained a significant focus for the major banks’ management teams in 2024. While cost drivers continue to be largely aligned to strategic focus areas, including cloud-based technologies, cyber security costs and continued investments in technology infrastructure and new technologies, currency weaknesses in African markets outside South Africa offset ZAR-based cost growth. Overall, the pace of cost growth (4.7%) marginally exceeded revenue growth (4.2%), resulting in the aggregate cost-to-income ratio increasing to 52.9% (FY23: 52.4%).

- ROE and capital: Similar to our observations in the first half of 2024, the volatile currency effects of translating foreign operations impacted the major banks’ combined ROE which fell 15 bps to 17.5% (FY23: 17.6%). This outcome is however still reflective of positive economic leverage as the combined ROE remains above the major banks’ average cost of equity of 15%. Although the combined common equity tier 1 capital ratio moderately increased to 13.3% (FY23: 13.2%), the major banks are aware of the need for ongoing capital optimisation strategies in light of new prudential regulatory reforms that take effect in 2025.

“The major banks have demonstrated their ability to navigate a complex and uncertain environment with resilience and effective strategic focus. As we look ahead, their commitment to innovation, sustainability and customer-centricity will remain central to their overall bank strategies for unlocking growth and delivering value.”

Outlook: The IMF notes in its January 2025 World Economic Outlook Update that prospects for global growth are considered divergent and uncertain, with forecast global growth expected to remain stable, but lacklustre, at 3.3% in both 2025 and 2026. Importantly, the report notes that “trade headwinds—including the sharp uptick in trade policy uncertainty—are expected to keep investment subdued.”

In South Africa, sharp focus shifted to the nation’s urgent need for growth and its fiscal position following the sudden postponement of the Budget Speech, which subsequently took place on 12 March 2025. Our theme for Budget 2025/2026, ‘Responsible growth for a sustainable future’, captures the need for the right fiscal choices today in the interest of South Africa’s tomorrow. While the 0.5% increase in the VAT rate in 2025 and 2026 will negatively impact consumers, it is part of a strategy aimed at righting the country’s fiscal ship.

Meanwhile, the SARB cut its key interest rate by another 25 basis points to 7.50% at the end of January 2025, marking the third successive reduction. While inflation remained well-contained, the medium-term outlook is more uncertain than usual.

As 2025 unfolds, South Africa’s major banks remain focused on the dual priorities of navigating a challenging environment while capturing appropriate opportunities. Building on the resilience demonstrated in 2024, key focus areas in 2025 are likely to include:

- Interest rate relief and credit growth: Within the context of an anticipated rate cutting cycle, the major banks are poised to benefit from stimulated lending activity, particularly in the retail and small business segments, and reduced impairment pressures.

- Digital leadership and innovation: The customer tilt to digital banking continues to accelerate, with investments in AI, cloud technology and cybersecurity remaining centre stage. We expect to see the major banks further enhancing customer experiences, streamlining operations and leveraging data and enhanced analytics to drive personalised financial services delivery and internal efficiencies.

- Sustainable finance and climate transition: Sustainability remains a core focus, with the major banks looking to build on their sustainable financing portfolios as global climate goals remain priorities. This includes funding green infrastructure projects and initiatives that seek to manage climate-related risks in vulnerable sectors.

- A decisively pan-African focus: The major banks’ operations across high-growth African markets remain critical engines of growth. Despite currency volatility and regulatory challenges, strategic investments in these regions continue to diversify revenue streams and competitive positioning.

- Cost management and efficiency: Disciplined cost control will remain a priority, particularly against potentially renewed inflationary pressures on the back of recent global trade dynamics and tariff threats. The major banks have all clearly stated their intentions to optimise their cost-to-income ratios through, inter alia, technology-driven efficiencies and targeted investments in talent and infrastructure.

South Africa’s major banks are well-positioned to balance short-term challenges with medium- to long-term growth opportunities. Leveraging their track record of resilience and innovation—including the strength of their franchises—is likely to guide their value propositions for customers and stakeholders in a highly complex and uncertain operating environment.

Contact us

Partner | Banking and Capital Markets, PwC South Africa

Tel: +27 (0) 11 287 0610

Francois Prinsloo

Banking and Capital Markets Industry Leader, PwC South Africa

Tel: +27 (0) 11 797 4419

Rivaan Roopnarain

Partner | Banking and Capital Markets, PwC South Africa

Tel: +27 (0) 11 287 0915