South Africa’s major banks continue to exhibit growth and resilience amidst complex conditions and considerable uncertainty.

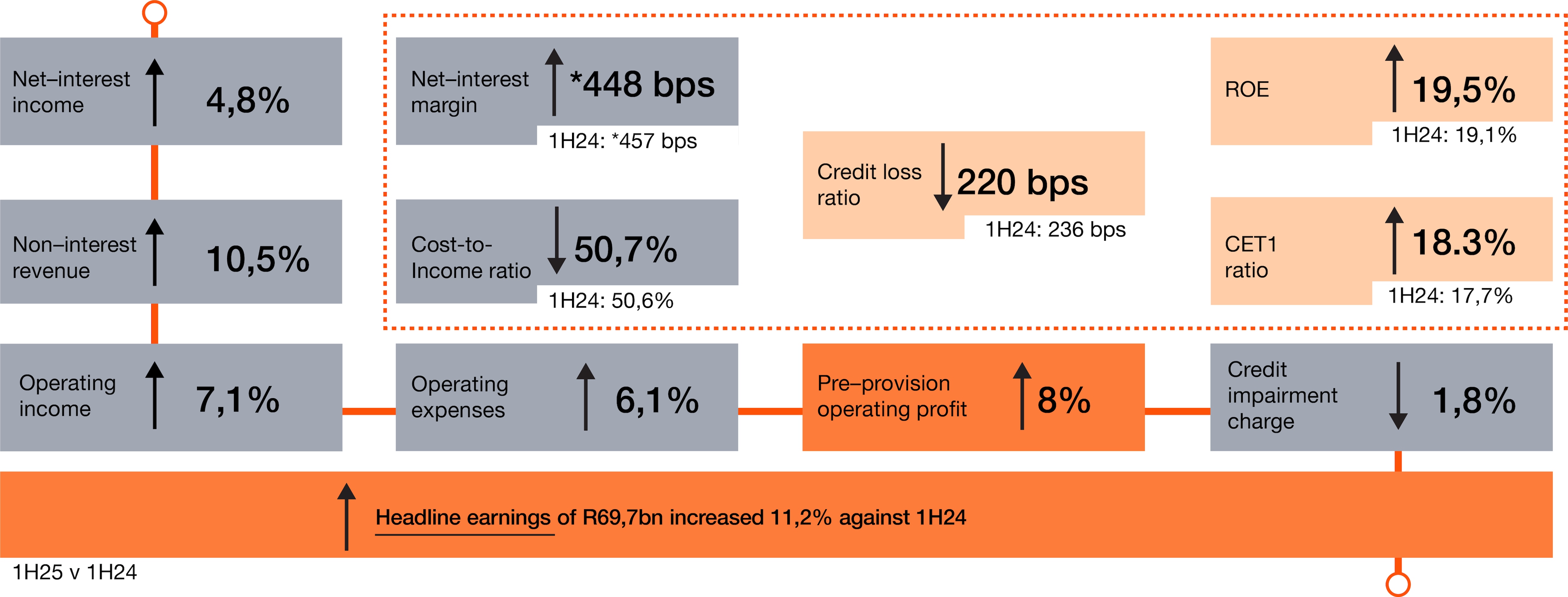

Combined headline earnings growth of 11.2% against 1H24 to R69.7bn, combined ROE of 19.5% (1H24: 19.1%), net interest margin of *448 bps (1H24: *457 bps), credit loss ratio of 220 bps (1H24: 236 bps), cost-to-income ratio of 50.7% (1H24: 50.6%), common equity tier ratio of 18.3% (1H24: 17.7%)

*Excluding Capitec

The first half of 2025 was a period of strategic navigation for South Africa's major banks. Operating against a backdrop of mixed global growth, persistent geopolitical tensions, major trade uncertainties and gradual shifts in monetary policy, the major banks results reported in 1H25 reflect their position as pillars of financial stability. These results are the product of well-executed strategies refined over several periods: strategies which blend defensive strength in capital and risk management while investing in digital transformation and further unlocking regional opportunities.

Commenting on the major banks’ results for the period, Rivaan Roopnarain, PwC South Africa Banking and Capital Markets Partner, notes, “The defining narrative accompanying the major banks results for the first half of 2025 is one of disciplined strength. While operating conditions remained complex, characterised by low domestic growth and amplified by shifts in the geopolitical landscape and global trade uncertainties, the major banks’ management teams navigated the period honing their strengths, enhancing customer experiences and capitalising on opportunities to further extract efficiencies.”

As we have previously noted, the major banks’ financial results do not occur in isolation. They are the output of a range of decisions made by bank management every day and their navigation within the broader economic environment in which they operate. In analysing their results, we focus on where they have been channelling their energies and what their next priorities may be. Several of those priorities could help to strike a balance between stability (financial and operational risk management) and agility (adapting products to evolving customer preferences and adjusting capital and liquidity positions to cater for global market volatility). The major banks’ robust financial performance reported in this period reflects these priorities across several common strategic themes, including:

- Digital foundations: The major banks continue transitioning and refining their core systems on cloud platforms, modernising payments across Africa, and unifying systems into single hubs. The value delivered is speed: new products that previously took months to launch are now delivered in weeks, while compliance with evolving local and global standards and regulations is increasingly built into product and system development cycles. This agility allows banks to adapt to customer expectations with greater responsiveness. At the same time, use cases of emerging technologies like generative artificial intelligence continue to be analysed in terms of potential impacts and opportunities internally and on their customers. While the major banks have previously commented on the need to leverage artificial intelligence in a responsible manner, potential use cases continue to expand into areas such as retail credit-scoring models, fraud engines that flag suspicious activity faster, and chatbots that can resolve almost all basic customer and employee queries with minimal human intervention. The benefits: safer transactions and service at scale without inflating operating costs.

- Customer experience at the core: With increased retail banking competition, driven by newer entrants, the primary arena of daily customer banking experiences is now decisively mobile and online channels, with the number of digitally active clients reaching record levels in this period. Consequently, we continue to observe banking applications increasingly being designed around making customers’ lives easier by expanding the range of value-added services available on banking apps, payments optimisation, and broader and faster product delivery. African banking customers are also accustomed to real-time insights powered by data and analytics-based intelligence, suggesting better ways to save or having problematic spending patterns flagged, while in-app biometrics and secure messaging make the experience both safer and more human. The result is financial platforms that are embedded in customer’s day-to-day experiences. Therefore, it is clear why the major banks continue to reference how AI is making, and will continue to make, customer experiences more seamless and engaging. Meanwhile, cybersecurity investments are being scaled up proportionally, reflecting the major banks’ recognition that digital trust is the foundation of the modern banking relationship.

- Robust balance sheets: South Africa’s major banks have routinely shown their capacity to move beyond compliance with prudential regulatory standards towards sophisticated financial resource optimisation. Advanced analytics are now increasingly used to dynamically allocate capital to drive risk-adjusted-returns, while stress-testing scenarios are expanding to include a wider range of geopolitical, climate-related and other emerging risks. Against this context, the major banks’ balance sheets remain anchored by strong capital, liquidity and risk management positions.

- Franchise strength: Resilient loan growth (up 6.4% against 1H24) combined with strong deposit taking (up 10.6% against 1H24) across customer and product segments provided the foundation to support earnings growth in 1H25. In response to competitive pressures brought about by newer market entrants and banking-adjacent financial services competitors, the major banks continued to focus on customer-first strategies and leveraging their established brands. Headline earnings growth was sustained by a combination of solid revenue growth (in both net interest income and non-interest revenue), sturdy cost control and a marginal decline in credit impairment charges over the period. However, strong competition for quality assets placed pressure on margins, evident in the relative contraction of the combined net interest margin.

- Capturing continental growth remains key to overall bank strategy: The pursuit of growth across sub-Saharan Africa remains a central mission of most of the major banks. Growth from businesses across Africa have continued to increase as the major banks continue to leverage technology and innovation and adapt operating models to challenge and reinvent their business models. While currency volatility presents a persistent headwind, the underlying strength of operations of those banks with a broad regional presence—serving young, dynamic, digitally-native populations—allows them to continue diversifying revenues and solidifying their pan-African corporate identities. A constant theme evident in this and recent results is that those banks with sizable portfolios in sub-Saharan Africa saw earnings benefit from regional diversification. Strong corporate and investment banking performances driven by advisory fees and trading activity in African territories outside South Africa, together with partnerships with fintechs and mobile money operators to gain scale and local expertise more efficiently, helped offset softer growth in some parts of their South African operations. However, domestic economic concerns in several African countries—compounded by currency volatility and varying tariff impacts—translated into elevated sovereign risk outlooks. We note, therefore, that some major banks increasingly measure success in constant currency terms to better assess underlying business performance without the noise of foreign exchange volatility.

- Optimising operating models: Rather than organising themselves strictly by legal entity or product set, some banks have begun pivoting to group-wide segment-based operating models. This allows for the concentration of talent, systems, technology investment and product innovation where customer demand is the greatest, while preserving scale efficiencies in back-office and shared services. For example, sustainable financing is transitioning from the domain of corporates only to becoming an integrated part of the overall banking product suite across business, commercial and retail banking clients. This includes green bonds for renewable energy projects, sustainability-linked loans that offer preferential terms for meeting ESG targets, preferential financing arrangements for off-grid utilities, and developing risk models that more accurately price climate-related physical and transition risks. Other operating model shifts observed in recent periods include combining private banking with wealth management and bringing small to medium-sized enterprise business banking closer to retail banking. The latter reflects the reality that entrepreneurs often operate as both individuals and business owners, requiring financial services that cross over—such as linking personal savings to business lending, or using a single app to manage household budgets and business cashflow. The benefits are simpler, more intuitive experiences for clients and greater cross-selling opportunities for banks.

- Major banks’ results highlights: PwC’s Major Banks Analysis highlights key themes from the combined local currency results of Absa, Capitec, FirstRand, Nedbank and Standard Bank which these banks published during 1H25. We also provide reflections from the common strategic themes within other South African banks. For this period, all comparative figures were restated to incorporate Capitec into our analysis, which includes their published results for the period ended 28 February 2025. The South African operations of the major banks included in our analysis comprised 85% of total banking sector assets in South Africa (based on June 2025 BA 900 industry data).

*Net interest margin excludes Capitec

“South Africa’s major banks continue to prove that they are amongst the most dynamic and innovative organisations globally. It comes as no surprise that they are recognised on a global scale for innovation in product depth, transaction banking, small and medium enterprises solutions, and digital innovation. Their results reported in the first half of 2025 reflect the careful orchestration of their strategies and responses to rapidly shifting economic, technological and customer trends.”

- Headline earnings: The major banks’ combined headline earnings growth of 11.2% against 1H24 to R69.7bn significantly outpaced the rates of economic growth in South Africa and sub-Saharan Africa. Underpinning earnings growth was the combination of solid top-line growth across net interest income (up 4.8% against 1H24) and non-interest revenue (up 10.5% against 1H24), supported by a nearly 2% decline in bad debt charges.

- Loan formation: Reflecting moderately improved, although cautious, consumer and business sentiment in the first half of 2025, new loan disbursements supported aggregate gross loans and advances growth of 6.4% against 1H24 (2.6% against 2H24). As always, individual loan portfolios and industry sectors showed differentiated growth rates between the major banks, based on a combination of differing strategies, geographic profiles and risk appetites. Based on Bureau information from the National Credit Regulator (NCR), the number of credit-active South African consumers increased to 28.9 million at the end of March 2025, growing 3.5% year-on-year. Although the interest rate hiking cycle seen in previous periods has abated, the cumulative impact of recent rate increases and their lagging effect weighed on household disposable income in the period, leading to softer credit demand in certain retail and commercial portfolios.

- Credit quality: The combined credit loss ratio (the income statement impairment charge divided by average advances) moderated to 220 bps (1H24: 236 bps) as the bad debt charge decreased by 1.8%. While the credit loss ratio of most of the major banks benefitted from product and geographic diversity, retail unsecured lending portfolios exhibited features of higher risk costs in this period. Total non-performing loans increased 3.4% against 1H24, comprising 5.6% of gross loans and advances (1H24: 5.8%). According to the NCR Bureau information noted above, the number of South African consumers with impaired records in Q1-25 increased by 196,181 to 10.41 million, while consumers classified in good standing increased by 92,475 to 18.49 million.

- Costs: As Stats SA notes, “After holding steady at 2.8% in April and May, consumer inflation edged higher to 3% in June.” This trend continued for a second consecutive month in July. In certain key territories in which some of the major banks operate in the rest of Africa, inflation trajectories remained volatile. Against this backdrop, cost management remained a central focus for the major banks’ management teams in the first half of 2025. Cost drivers continue to be aligned to strategic focus areas, including innovation and technology investments and advancing cyber defences. Overall, the pace of cost growth (up 6.1% against 1H24) was managed below operating income growth (up 7.1% against 1H24), resulting in the aggregate cost-to-income ratio remaining essentially flat at 50.7% (1H24: 50.6%).

- ROE and capital: On a combined basis, the major banks reported ROE for the period increased 40 bps to 19.5% (1H24: 19.1%). This outcome remains reflective of positive economic leverage as the combined ROE remains above the major banks’ average cost of equity. Admirably, the combined common equity tier 1 capital ratio expanded to 18.3% (1H24: 17.7%). Capital management strategies are likely to remain an area of focus for management teams in light of new prudential regulatory reforms that took effect from 1 July 2025.

“The major banks continue to demonstrate agility in operating in complex conditions. The migration of nearly 21 million clients to digital platforms is now the central fact of retail banking in South Africa and the rest of the continent. In response, the major banks continue to evolve to market and customer trends–while fortifying cyber defences and overall IT resilience–by crafting personalised customer experiences that anticipate needs and erase friction.”

Outlook: Looking ahead for the rest of 2025, the global environment is expected to remain volatile and complex to anticipate, with divergent growth prospects between territories. The impact of trade tariffs, volatile commodity prices and varying inflation trends are all expected to complicate monetary policy decisions and rate forecasting, while potentially constraining business sentiment.

Domestically, the economic outlook hinges on the steady implementation of structural reforms. Easing inflation is expected to allow for modest interest rate cuts in the latter half of the year, providing some relief to consumers. However, meaningful economic improvement is contingent on tangible progress in resolving South Africa’s structural constraints, including in logistics networks spanning ports and rail. The consensus outlook among the major banks settles on a slow, structurally limited uplift for South Africa’s short-term growth prospects.

South Africa's major banks have entered the second half of 2025 from a position of strength. Their 1H25 financial performance is a testament to disciplined strategy execution that prioritises long-term resilience. By successfully managing immediate pressures while investing in the foundational technologies and strategies required for future growth, they continue to demonstrate a sophisticated understanding of their role in a dynamic African economy. For the rest of 2025 and over the medium term, we continue to expect South Africa’s major banks to remain seized with executing on their strategies with intent, with key focus areas likely to remain:

- Monetary policy normalisation: Market consensus anticipates further gradual rate cuts from the SARB. Banks will likely continue their sophisticated balance sheet management actions to protect margins, focusing on non-interest revenue streams and cost management activities to support earnings growth.

- Data as a strategic asset: The next competitive battleground is likely to be the use of data. Those banks that best leverage customer data—within stringent personal information privacy frameworks—to create hyper-personalised products, improve credit scoring, and enhance customer service will pull ahead, particularly given the demographics of the continent.

- Regulatory change: Dramatic shifts in the geopolitical landscape largely had a minimal direct impact on the major banks’ reported results in this period. However, regulatory guardrails to ensure capital and operational resilience are either embedded or well underway. South Africa’s adoption of Basel III, including the recent post-crisis reforms which came into effect on 1 July 2025, reflects its commitment to globally leading prudential standards. While the major banks will continue to be focused on the operationalisation of these new regulatory reforms, their planning for this has been several years in the making.

The major banks will continue to counterbalance immediate challenges with growth opportunities. The foundations underpinning their resilience—including advanced risk management capabilities and strong levels of capital and liquidity—provide the basis for them to remain focused on unlocking internal efficiencies, making customer experiences more frictionless and capturing opportunities brought about by emerging technologies.

Contact us

Partner | Banking and Capital Markets, PwC South Africa

Tel: +27 (0) 11 287 0610

Francois Prinsloo

Banking and Capital Markets Industry Leader, PwC South Africa

Tel: +27 (0) 11 797 4419

Rivaan Roopnarain

Partner | Banking and Capital Markets, PwC South Africa

Tel: +27 (0) 11 287 0915