Introduction

PwC’s South Africa Telecommunications Sentiment Index—developed in partnership with DataEQ—is South Africa’s most robust analysis of telecom customer experience, with metrics specifically designed for the telecoms industry. For the first time, it goes beyond traditional Network Providers (NPs) to include Fibre Network Operators (FNOs), Internet Service Providers (ISPs) and Mobile Virtual Network Operators (MVNOs). The insights from this report enable telecom leaders to uncover the root causes of customer dissatisfaction and benchmark performance across the broader industry.

"In a connected, converging world, improving customer service is a springboard for telecoms into new markets, new business models and untapped growth."

Methodology

The index analyses of public online conversations across major telecom brands to gauge sentiment and uncover key perceptions. Posts are categorised as either operational (e.g. seeking support or giving feedback on service, products or networks) or reputational (e.g. brand perception, reaction to campaigns). Net Sentiment scores reflect the balance of positive and negative conversation.

Operational posts are especially important as they represent real customer needs and often signal purchase intent or cancellation threats.

Data sources analysed:

- X (excludes DM conversations)

- Hellopeter

- Websites

- Facebook (only for Network Providers)

Subsector breakdown:

| Network Providers (NPs) | Fibre Network Operators (FNOs) | Internet Service Providers (ISPs) | Mobile Virtual Network Operators (MVNOs) |

| Licensed operators that own spectrum and/or mobile infrastructure. They deliver mobile voice and data services directly to consumers | Providers that build and manage fixed-line infrastructure (specifically fibre networks) used to deliver high-speed internet. | Brands that offer internet access to customers, typically by leasing infrastructure from FNOs. They manage the customer relationship and service delivery. | Brands that lease mobile network capacity from NPs to offer mobile services under their own name. They don’t own infrastructure but compete on pricing, service and innovation. |

|

|

|

|

Index ranking highlights

Rain retains its position at the top of the network provider category, while Cell C shows real momentum with a sharp year-on-year sentiment lift. Telkom Fibre was the only ISP to achieve a positive public Net Sentiment, with praise for reliable connectivity and innovative prepaid fibre products. FNO Openserve earned solid sentiment for its reliable infrastructure and efficient service delivery. MVNOs are gaining ground—led by Capitec Connect with an impressive +88% Net Sentiment—driven by simplified offerings and agile digital experiences.

These are the standouts—top performers and key movers across the index:

Key report findings

1. Operational issues are costing telecoms their customer loyalty

Customers are hitting roadblocks when trying to cancel, query bills or activate SIMs. Traditional service lines—call centres, branches and email—are underperforming. Long wait times and unreliable service channels are pushing customers to look elsewhere.

2. Campaigns spark interest—but service seals the deal

Industry-wide reputational sentiment stood at +25%, driven by campaign-led engagement. Marketing activations are clearly driving reputational wins. But without operational follow-through, these sentiment gains are short-lived.

3. ISPs and FNOs must close the accountability gap

ISPs recorded the most negative sentiment, with complaints about outages, billing and poor digital support. FNOs faced similar issues, compounded by unclear handoffs and blame shifting between ISPs and FNOs. Openserve stood out with positive sentiment, thanks to reliable infrastructure and proactive communication.

4. When the network drops, so does trust

Connectivity complaints are some of the top drivers of negative sentiment, with a -87% industry-wide net sentiment for network quality. Customers are frustrated by unstable signals and unusable data. The fix is clear: proactive communication and smarter outage resolution.

5. Digital support cuts costs, complaints and churn

With a -89% overall industry net sentiment, poor digital experiences are driving customer frustration and cancellation intent. Improving digital support is the most cost-effective way for telecoms to cut complaints, ease contact centre pressure and unlock smarter services.

6. MVNOs are winning hearts—and market share

MVNOs are winning on sentiment, thanks to simplified offerings, agile digital experiences and influencer-led campaigns. But sustaining momentum will require consistent service delivery, not just marketing flair.

“In a saturated and ever-evolving telecoms market, service and personalisation speak loudest—it’s a strategic advantage. With standout players now showing what’s possible, there’s real momentum to build on. Let’s make it count.”

Industry sentiment overview

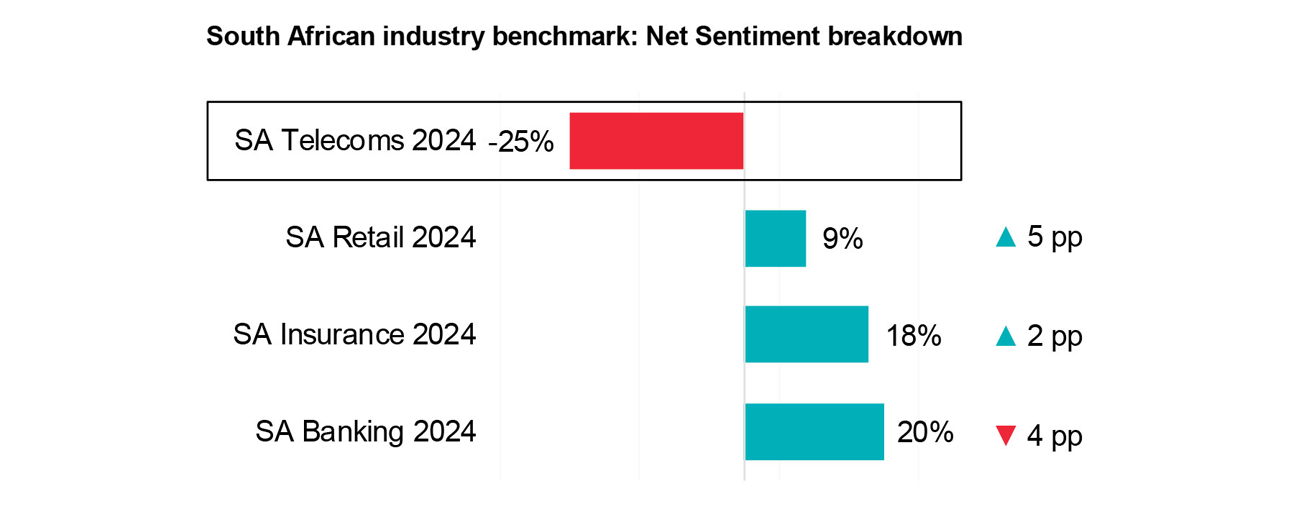

South Africa’s telecoms industry faced notably more negative discussion than any other industry

Source: DataEQ and PwC analysis

South Africa’s telecoms sector is under pressure, recording an overall Net Sentiment of –25%. Telecoms was the only industry where negative sentiment outweighed the positive: this was apparent across network providers, ISPs and FNOs.

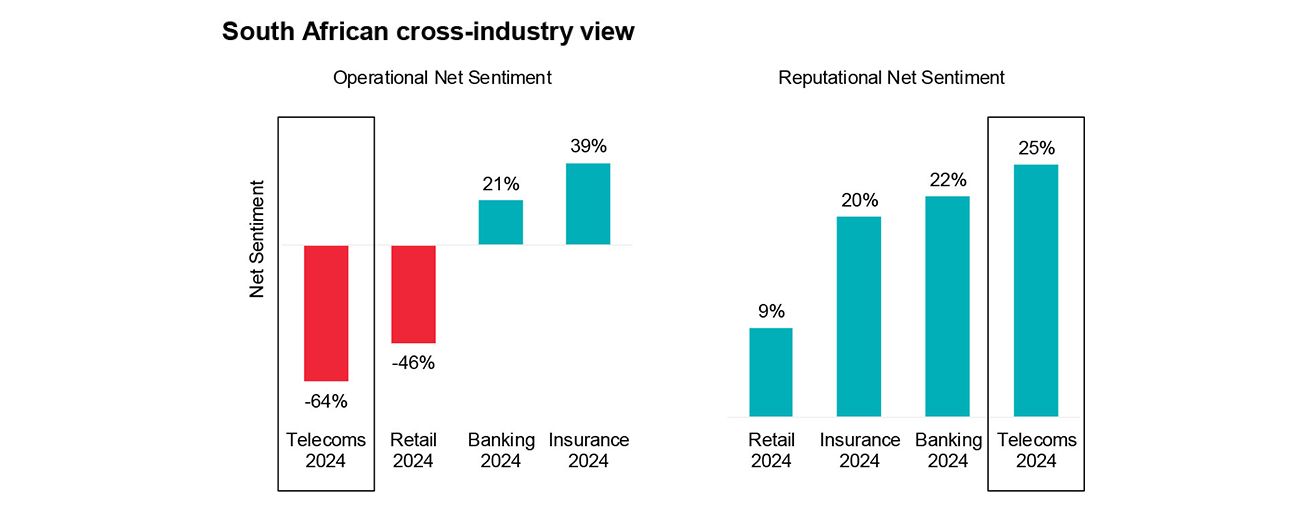

Campaigns cushion customer complaints

Source: DataEQ and PwC analysis

Telecoms scored highest on reputational net sentiment, thanks to high-impact campaigns and brand partnerships. But these wins are masking deeper service issues. Operational net sentiment is the lowest across all industries and was impacted by complaints linked to poor network quality and customer service.

Service sentiment reveals the real gap

Across industries, serviceable posts are a clear barometer of customer experience. Telecoms recorded the lowest Net Sentiment in this space, with widespread frustration over billing errors, outages and poor responsiveness. Retail was an outlier, achieving a positive score by turning service interactions into opportunities—leveraging promotions and offers to drive positive operational conversation.

Lessons from leading industries

South African banks are setting the benchmark with emotionally resonant campaigns and strategic partnerships that drive both reputational and operational uplift. Insurers are converting service excellence into industry-leading operational sentiment. Retailers, despite operational challenges, are maintaining reputational strength through loyalty programmes and brand collaborations.

Campaigns can drive operational positivity Banks and insurers didn’t just rely on reputational campaigns—they used targeted, product-focused content to improve operational sentiment. |

Lesson for Telecoms: Don’t limit campaigns to brand awareness. Use them to spotlight service wins, educate customers on processes (like billing or cancellations) and invite feedback on improvements. |

Visible responsiveness builds trust Insurers earned positive sentiment by visibly closing the loop on customer feedback—especially on platforms like Hellopeter. Public resolution signals not only reassure existing customers— but also influence potential ones who now use these platforms to compare service quality and responsiveness. |

Lesson for Telecoms: Encourage satisfied customers to share their experiences on public platforms. Show up in the conversation. When telecoms respond directly to feedback—especially after resolution—they signal accountability and care. That’s what builds credibility. |

Digital experience is a shared weakness and a shared opportunity Retail and telecoms both struggled with digital service channels. However, where retail is now investing in delivery tracking, app UX and real-time support, most telecoms still lag. |

Lesson for Telecoms: Digital is the fastest fix. Prioritise app stability, chatbot responsiveness and proactive notifications to reduce pressure on call centres and improve customer satisfaction. |

Subsector sentiment comparison

Source: DataEQ and PwC analysis

Network providers, FNOs and ISPs all faced heavy criticism for poor connectivity, slow issue resolution and weak support. Serviceable interactions were overwhelmingly negative, with ISPs recording the worst public net sentiment due to long wait times and poor communication. Network providers fared better, but reputational praise masked persistent operational complaints. Fibre operators were caught in the middle, often blamed alongside ISPs for outages and delays.

Source: DataEQ and PwC analysis

Source: DataEQ and PwC analysis

Network Providers recorded public Net Sentiment of -8%, with rain and MTN achieving positive scores. Operational sentiment sat at -49% (above the telecoms industry aggregate of -64%), while reputational sentiment reached 23%.

rain kept hold of the top spot with a net sentiment of 11% and led both reputational and operational categories. MTN saw reputational gains through its #MTNSummer campaign. Telkom and Cell C also generated positive reputational sentiment through creative activations. Despite improvements, contract-related complaints and poor support from brand agents remain key challenges across the subsector.

The network providers subsector reached a five-year sentiment high, driven mainly by a reduction in complaint volumes and a rise in campaign-led positivity. Despite the overall negative score for the subsector, all but one network provider showed improvement from the previous year. Cell C had the largest year-on-year net sentiment improvement at 29%.

ISPs faced the most negative sentiment across the industry, with public net sentiment at -48% and operational scores at -72%. Reputational sentiment was however the highest in the industry at 30%.

Complaints focused on outages, installation delays, pricing dissatisfaction and poor digital experience. The strong reputational performance was driven by isolated well-executed competition campaigns and reshares of promotional posts.

Telkom Fibre was the only ISP to achieve a positive public Net Sentiment (2% —significantly higher than the subsector aggregate of -48%). Telkom Fibre was praised for reliable connectivity and its R99-per-week prepaid fibre product.

FNOs recorded public net sentiment of -30% and reputational sentiment of 29%. Operational sentiment was the worst in the industry at -73%.

FNO customers struggled with outages, poor connectivity and unclear accountability. Customers often blamed both ISPs and FNOs for service failures, pointing to a shared responsibility gap.

Openserve was the only FNO to achieve positive sentiment, leading both operational and reputational scores. Its net sentiment score of 24% is significantly higher than those of its FNO peers and the subsector average of -30%. Its affordable fibre products, community outreach and efficient service delivery helped it stand apart.

Customer experience drivers

Contract-related issues were the biggest driver of dissatisfaction (–80%). Customers struggled with cancellations, billing disputes and SIM activations. Some felt misled by staff, citing inadequate explanation of contract terms and conditions before signing. Customers frequently flagged issues where poor connectivity made it difficult to use their airtime and data bundles as intended. Unresponsive digital channels, log-in issues and unsuccessful online airtime transactions came in for criticism.

The ISP sector recorded the lowest Net Sentiment for serviceable posts across all telecom categories. Customers reported long installation/activation delays, issues with faulty or missing hardware equipment and setup challenges. Pricing remained a major driver of negative sentiment, particularly where users experienced billing discrepancies, slower-than-advertised internet speeds, and misleading advertising around delivery or setup fees. ISPs had the lowest Net Sentiment in the index for Digital Experience, at -92%. Inefficient digital channels and glitchy self-service indicates a broader need for investment in digital responsiveness.

Despite being the most responsive category in terms of ‘reply’ rates, FNOs still recorded highly negative service sentiment due to connectivity failures, unresolved outages and poor communication. Customers cited ticket closures without resolution, extended delays in installation or activation and general unresponsiveness. In some cases, users said they had paid for services that never became operational leading to heightened frustration, particularly when outages disrupted work or business activity. Confusion during fibre transitions and unclear handoffs between providers led to service gaps.

Traditional service channels fall short in the eyes of customers

Source: DataEQ and PwC analysis

Traditional support channels: Stuck. Slow. Struggling

Traditional service channels—call centres, branches and email—are driving dissatisfaction across telecoms. Customers cite no responses, slow responses, inaccurate information and unhelpful agents—especially when reporting technical issues.

Digital platforms aren’t delivering either

Digital platforms like WhatsApp and mobile apps had lower volumes but were also negatively perceived. Websites and mobile apps are under fire for login failures, password reset issues and unreliable OTPs. In-app data or airtime purchases often fail, and users also report difficulty cancelling services. Live chat and WhatsApp support were criticised for bot-like interactions, long response times or no replies at all.

Signal strain: How network quality is driving customer churn

Across South Africa’s telecom landscape, network quality has emerged as a main source of customer dissatisfaction, mentioned in 16% of serviceable conversation. Whether through dropped connections, unsatisfactory issue resolution or vague outage communication, consumers are losing patience and providers are losing trust. A handful of providers showed signs of progress, but the broader industry continues to fall short of customer expectations, with an overall network quality net sentiment at -87%. The sentiment gap between subsectors was narrow, with all scoring close to the average.

Cell C defies the odds

Network provider customers reported unstable signal, persistent connectivity failures and unusable data despite active bundles. Cell C outperformed the subsector Net Sentiment of -84% by 16 percentage points (-68%). Customers noted improved stability and coverage, suggesting targeted investments are starting to pay off.

Cool Ideas cushion a poor ISP average sentiment

With a Net Sentiment of -87%, ISPs faced backlash over prolonged outages, long technician wait times and poor communication. Cool Ideas (-78% network net sentiment) outperformed the ISP average by 9% lifting the ISP average sentiment slightly.

Fibre frustrations fuel cancellations

FNOs recorded the lowest subsector Net Sentiment at -89%, driven by multi-day outages and generic support responses. Customers want root-cause resolution, not scripted, generic troubleshooting. FNOs were also tagged in 20% of ISP network complaints, illustrating the importance of ISP/FNO collaboration in communicating and resolving outages.

What drives customers to join—or leave?

Across the industry, poor network quality and contract issues were widely cited cancellation drivers. Contract cancellations were often described as intentionally difficult and obstructive, with unhelpful agents, delayed responses, branch-level restrictions, early cancellation fees and continued billing after cancellations. Network performance issues directly motivated requests to switch providers.

Network Providers won acquisition interest through mobile device hardware promotions and data SIM deals. Vodacom’s R249 4G cloud smartphone drove a lot of interest. rain led the charge in mobile internet and router interest with its smart router offering. MTN led in contract-driven acquisition conversation, driven by Gold Plan and home fibre offers.

ISPs poor digital experience sentiment was reflected in cancellation threats over issues such as failed WhatsApp support. Telkom Fibre enjoyed more purchase conversation than any other provider, with potential customers enquiring about pricing and area coverage. Afrihost sparked the interest of consumers looking for a more reliable ISP.

FNOs were associated with ISPs when users faced prolonged uncommunicated outages and unresolved router issues leading to cancellation requests.

Digital experience is a weak link—and a fast fix

Digital customer support didn’t just show up as a weak spot—it cut across multiple pain points. It was flagged as a service channel issue, with lower usage but consistently poor sentiment. It was the most negatively rated customer experience driver across the industry, at -89%. And for ISPs, it formed part of cancellation intent conversation.

Yet, this is also where the biggest opportunity lies. When implemented well, digital channels can ease pressure on underperforming contact centres and branches, offering faster, more scalable support. Improving digital service reduces operational costs, thanks to automation and self-service. Digital channels also generate rich data on behaviours, pain points and preferences that can be used to continuously improve customer experience.

MVNOs: A lesson for legacy operators?

MVNOs offer a glimpse of what good can look like. Their rapid growth and strong sentiment scores show what’s possible when marketing meets digital agility. But sustaining that momentum means moving beyond campaigns to consistent customer experience.

Capitec Connect (South Africa’s largest MVNO) led both in volume and overall Net Sentiment at 88%. A well-executed campaign encouraged users to tag friends and share reasons to switch. Capitec Connect’s quick subscriber growth was also widely praised.

MVNOs are also winning on digital experience. Their smoother onboarding and personalised features (like eSIMs and flexible month-to-month plans) contributed to positive sentiment.

The MVNO sector’s success in driving both operational and reputational positivity, especially through targeted campaigns and influencer engagement, sets a marketing benchmark for the broader industry. However, when campaign-driven conversation was removed, Operational Net Sentiment dropped by 104 points, shifting from strongly positive to negative (-39%, 10% above the operational Net Sentiment for network providers).

Customer complaints focused on SIM and network-related issues, including failed activations, poor coverage and porting delays. Many users also raised concerns about slow response times, poor communication, and unresponsive support. While some organic praise remained especially around affordability, friendly agents, and the fresh appeal of new entrants, maintaining long-term sentiment will depend on the ability to deliver consistent service beyond campaign spikes.

MVNOs must now match their marketing efforts with consistent service delivery.

From signal to strategy: Turning sentiment into action

Customer sentiment remains a critical performance signal

The data is clear. Service failures are costing trust, loyalty and growth. From cumbersome cancellations to digital dead ends, South Africa’s telecoms sector is facing challenges that can’t be ignored. We’ve pinpointed the pain points. Now it’s time for action.

Agile players drive momentum

Agile players are already showing what’s possible: simplified offerings, smarter support and campaigns that connect. They’re not just adapting—they’re accelerating—and reinventing.

Digital is the fastest fix—and the smartest investment

AI-driven support, self-service apps and real-time support channels are outperforming traditional service lines. They’re cheaper to run, easier to scale and better at solving problems. But it needs to be done right. That means predictive support, intuitive platforms and real-time responsiveness. The opportunity is clear: scale digital before sentiment slips.

The path forward is pragmatic—and urgent

Telecoms must move from reactive fixes to proactive system design. That means embedding sentiment metrics into performance dashboards, scaling proven digital channels and aligning network reliability with customer-facing transparency.

“We help Telecoms transform with purpose: using data-driven insight to design customer experiences that connect, scale and deliver real impact.”

How we can help you

Subscribe to our mailing list

Subscribe to receive the next South African Telecommunications Sentiment Index publication

Contact us

Nana Madikane

Africa Technology, Media and Telecommunications Industry Leader, PwC South Africa

Tel: +27 (0) 11 797 5490

Basheena Bhoola

Partner | Telecommunication Specialist, PwC South Africa

Tel: +27 (0) 11 797 5687