PwC’s Major Banks Analysis highlights key themes from the combined local currency results of Absa, Capitec, FirstRand, Nedbank and Standard Bank which these banks published during 1H25. We also provide reflections on the common strategic themes within other South African banks.

For this period, all comparative figures were restated to incorporate Capitec into our analysis, which includes their published results for the period ended 28 February 2025.

The South African operations of the major banks included in our analysis comprised 85% of total banking sector assets in South Africa (based on June 2025 BA 900 industry data).

Download (PDF - 4.3MB) South Africa - Major Banks Analysis | September 2025

PwC's analysis of major banks' results reported during the first six months of 2025.

- South Africa - Major Banks Analysis | March 2025

- South Africa - Major Banks Analysis | September 2024

- South Africa - Major Banks Analysis | March 2024

- South Africa - Major Banks Analysis | September 2023

- South Africa - Major Banks Analysis | March 2023

- South Africa - Major Banks Analysis | September 2022

- South Africa - Major Banks Analysis | March 2022

Stability through uncertainty

South Africa’s major banks continue to exhibit growth and resilience amidst complex conditions and considerable uncertainty.

*Excludes Capitec

“The defining narrative accompanying the major banks results for the first half of 2025 is one of disciplined strength. While operating conditions remained complex, characterised by low domestic growth and amplified by shifts in the geopolitical landscape and global trade uncertainties, the major banks’ management teams navigated the period honing their strengths, enhancing customer experiences and capitalising on opportunities to further extract efficiencies.”

The major banks’ robust financial performance reported in this period reflects their priorities across several common strategic themes, including:

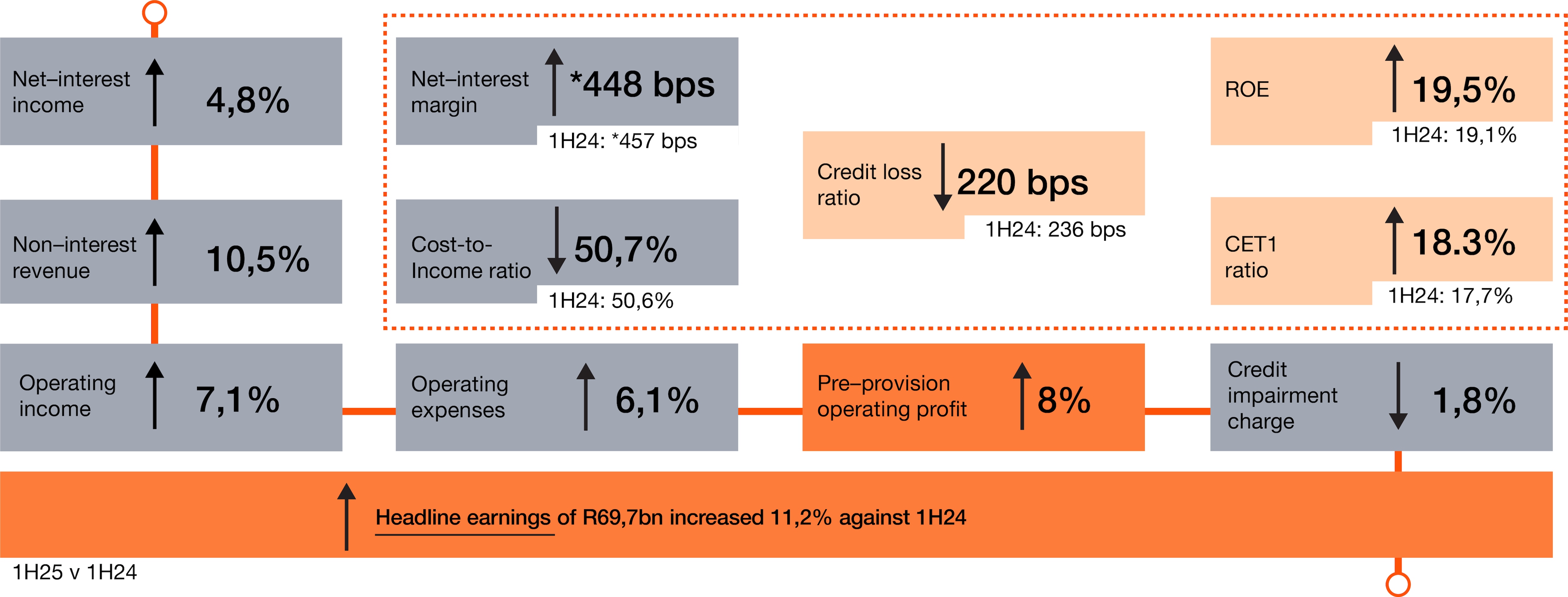

Summary of results

The first half of 2025 was a period of strategic navigation for South Africa's major banks. Operating against a backdrop of mixed global growth, persistent geopolitical tensions, major trade uncertainties and gradual shifts in monetary policy, the major banks’ results reported in 1H25 reflect their position as pillars of financial stability. These results are the product of well-executed strategies refined over several periods – strategies which blend defensive strength in capital and risk management while investing in digital transformation and further unlocking regional opportunities.

As we have previously noted, the major banks’ financial results do not occur in isolation. They are the output of a range of decisions made by bank management every day and their navigation within the broader economic environment in which they operate. In analysing their results, we focus on where the major banks’ have been channelling their energies and what their next priorities may be. Several of those priorities are aimed at striking a balance between stability (financial and operational risk management) and agility (adapting products to evolving customer preferences while adjusting capital and liquidity positions to cater for global market volatility).

*Excludes Capitec

“South Africa’s major banks continue to prove that they are among the most dynamic and innovative organisations globally. It comes as no surprise that they are recognised on a global scale for innovation in product depth, transactional banking, small and medium enterprise solutions, and digital innovation. Their results reported in the first half of 2025 reflect the careful orchestration of their strategies and responses to rapidly shifting economic, technological and customer trends.”

“The major banks continue to demonstrate agility in operating in complex conditions. The migration of nearly 21 million clients to digital platforms is now the central fact of retail banking in South Africa and the rest of the continent. In response, the major banks continue to evolve to market and customer trends – while fortifying cyber defences and overall IT resilience – by crafting personalised customer experiences that anticipate needs and erase friction.”

Outlook

Looking ahead to the rest of 2025, the global environment is expected to remain volatile and complex to anticipate, with divergent growth prospects between territories. The impact of trade tariffs, volatile commodity prices, and varying inflation trends is expected to complicate monetary policy decisions and rate forecasting, while potentially constraining business sentiment.

Domestically, the economic outlook hinges on the steady implementation of structural reforms. Easing inflation is expected to allow for modest interest rate cuts in the latter half of the year, providing some relief to consumers. However, meaningful economic improvement is contingent on tangible progress in resolving South Africa’s structural constraints, including in logistics networks spanning ports and rail. The consensus outlook among the major banks settles on a slow, structurally limited uplift for South Africa’s short-term growth prospects.

South Africa's major banks have entered the second half of 2025 from a position of strength. Their 1H25 financial performance is a testament to disciplined strategy execution that prioritises long-term resilience. By successfully managing immediate pressures while investing in the foundational technologies and strategies required for future growth, they continue to demonstrate a sophisticated understanding of their role in a dynamic African economy. For the rest of 2025 and over the medium term, we continue to expect South Africa’s major banks to remain seized with executing on their strategies with intent, with key focus areas likely to remain:

- Monetary policy normalisation: Market consensus anticipates further gradual rate cuts from the SARB. Banks will likely continue their sophisticated balance sheet management actions to protect margins, focusing on non-interest revenue streams and cost management activities to support earnings growth.

- Data as a strategic asset: The next competitive battleground is likely to be the use of data. Those banks that best leverage customer data—within stringent personal information privacy frameworks—to create hyper-personalised products, improve credit scoring, and enhance customer service will pull ahead, particularly given the demographics of the continent.

- Regulatory change: Dramatic shifts in the geopolitical landscape largely had a minimal direct impact on the major banks’ reported results in this period. However, regulatory guardrails to ensure capital and operational resilience are either embedded or well underway. South Africa’s adoption of Basel III, including the recent post-crisis reforms which came into effect on 1 July 2025, reflects its commitment to globally leading prudential standards. While the major banks will continue to be focused on the operationalisation of these new regulatory reforms, their planning for this has been several years in the making.

The major banks will continue to counterbalance immediate challenges with growth opportunities. The foundations underpinning their resilience—including advanced risk management capabilities and strong levels of capital and liquidity—provide the basis for them to remain focused on unlocking internal efficiencies, making customer experiences more frictionless and capturing opportunities brought about by emerging technologies.

Subscribe to our mailing list

Subscribe to future editions of the South Africa - Major Banks Analysis

Contact us

Francois Prinsloo

Banking and Capital Markets Industry Leader, PwC South Africa

Tel: +27 (0) 11 797 4419

Rivaan Roopnarain

Director | Banking and Capital Markets, PwC South Africa

Tel: +27 (0) 11 287 0915